Password policies are becoming more and more complicated all the time. Most policies nowadays require at least 8 characters both upper and lower case letters, at least one number and a special character. Some organizations can require up to 16 characters. The policy also requires that the password be changed on a regular basis and you cannot reuse any of the previous passwords or any parts from previous passwords.

What typically happens is people have a number of different long and complicated passwords for several different applications that they change fairly often so in order to keep track of them, they write them down somewhere where they won’t forget, undermining the purpose of having passwords. Even then there are times when we forget the passwords altogether and can’t find a note anywhere and we either have to go through the ‘forgot password’ process or we get locked out of our account.

The problem is how to have any number of arbitrarily long and complicated passwords, that have to be changed on a regular basis and not have to write them down, not worry about having to remember them and at the same time, make it as difficult as possible to interfere with social engineers looking over our shoulders.

“Password Automation and Declination” is a procedure which automates entering passwords which is complemented by augmenting the password entry with a declination pattern. In other words, the password entered is not in its final form, but rather its form must decline or be altered to find its final form.

Password Automation

In order to automate the introduction of the password, we can create a batch file with the following commands: ‘echo YourPasswordHere | clip’. This will automatically copy your password to your systems clipboard that you can then paste into the password field. Then you can create a shortcut to the batch file and assign a short-cut key combination that makes mnemonic sense. For example: CTR + ALT + B for your bank password or CTR + ALT + M for Gmail. The batch file and the short-cut can be hidden anywhere on your computer and they do not have to be together. Automation allows your password to be absolutely anything and when it has to be changed you just change it in the batch file.

Declination Pattern

The declination pattern is meant to add an additional authentication factor making it difficult for social engineers ‘looking over your shoulder’ to steal your credentials even if they are looking right at you. The declination pattern can be anything you want and should make sense to you so it’s easy to remember. Regardless what your password is, you can use the same declination pattern. A declination pattern means altering the original form of the password, the password template, in a particular order to produce the correct password before submitting it. It’s a set of ordered key: value pairs composed of indexes and actions denoted {index:action}. The declination can be deleting something, adding something or changing something at chosen indexes.

Let’s say you choose declination indexes 1 and 7, the indexes mean that after you enter your password in the password field, you will then decline the password form at index 1 and index 7 in that order. Let’s say delete the character at index 1 and add a character at index 7 in order to give us the correct password form for submission. Declination pattern {1:del, 7 ‘y’}. Applying the declination pattern in order matters since deleting characters can change the numbering of the indexes.

For example, if your password is ThisIsMyPassword2021!, then in the batch file you would put a valid password template for your chosen declination pattern. *ThisIsMPassword2021! is a valid template for the password ThisIsMyPassword2021! and declination pattern {1:del, 7: ‘y’} but anything that has a deleteable character in position 1 and is missing the ‘y’ at position 7 is valid. Applying the declination pattern {1:del, 7: ‘y’} then produces the password ThisIsMyPassword2021!. Password fields on web forms hide the characters in the password so the declination pattern is applied without anyone being able to see what characters in the password you are affecting. Your password could be any absurd, arbitrary monster like:

jdkf avyLLfldk adfj!@#$daj;f897 then a valid template for declination pattern {1:del, 7 ‘y’} to put in the batch file would be *jdkf avLLfldk adfj!@#$daj;f897 and that’s it. You never have to remember a single thing about it, just the short-cut keys and the declination pattern which haven’t changed.

Conclusion

Regardless how long and complicated a password is, all the user has to remember is the short-cut key to automatically copy the appropriate password template to the clipboard and the declination pattern. Even when the password changes to something completely new and long and complicated, there is nothing new to memorize. Just tailor the new password’s template in the batch file to fit your existing declination pattern and you can use the same short-cut keys.

The two factor nature of the procedure addresses the fact that, even if a social engineer sees which short-cut keys you use for the automation, it only gives him the password template and will be rejected if he tries to submit it. He would also need to know your declination pattern which is much more difficult for someone to pick up since they can’t see the password in the password field. The declination pattern is a pseudo-biometric in that it’s not something that has to be written down but rather just something meaningful to you that you remember.

This method not only accommodates large and complicated passwords that tend to change a lot, it invites them. The larger and more complicated the more effective the declination pattern.

If at any time the user thinks either his short-cut keys or declination pattern have been compromised he can simply change them. Declination patterns are extremely sensitive so the slightest change will prevent access.

The topic of Animal “Rights” attracts so much attention because it’s so asinine like a flat earth, man killing the planet or gender fluidity. It’s twenty-first century “civilized” society that more aptly resembles an insane asylum or a pre-school.

Rights require consent, so how do you get consent from an animal? You can’t, it’s impossible which means, if you believe animals have rights, you cannot do anything to an animal without violating its rights.

You cannot have pets, you cannot advocate people having pets and you cannot engage in any sort of animal rescue activities. It means all animals in the world should be wild and never interfered with by humans or other animals.

But if animals have rights, and they are violated by another animal, shouldn’t there be an “animal rights justice system”? Why don’t the animals have this? Why do they not hold the lion liable for murder when he kills the antelope?

This is the first of many perversions associated with this topic: animal rights are not animal rights at all, they are human rights projected onto animals, the anthropomorphism of the animal kingdom. But it’s a convenient, subjective anthropomorphism so as to appease socio-political agendas and people’s feelings.

They’ll argue animals have rights but they sure would like to take that cute little puppy from its mom to have as their own, they’ll even pay for it. Now where have I heard of rights being violated for money before? No it’ll come to me.

That’s the psychological fracture created from a lifetime of conditioning that allows them to claim animals have rights, while at the same time violating those rights by having animals as pets. Sold into what is tantamount to domesticated animal slavery without blinking an eye. Reducing the entire domesticated animal industry to nothing more than an animal slave trade writ large, but he’s wagging his tail so he must like it.

Tell me how did you get your pet’s consent to be domesticated? How did you get its consent to be vaccinated, castrated, micro-chipped, collared, leashed and fenced in? How do you get an animal’s consent to be euthanized, for its own good of course? So subjectively killing the animal is okay, just don’t eat it because it has rights! That’s a funny place to draw the line.

I always laugh when the “animal rights” activists claim they “rescued” a dog. Rescued him from what, freedom? This topic, like all such topics, requires an abandonment of all humanity. A complete and utter lack of reason, rational, logic and common sense. It’s an emotional response, not a rational one.

Emotionally, I’m an animal lover, always have been my whole life. I’ve had dogs, cats, hamsters, fish, my grandfather raised parakeets. Hell I can’t even kill a mouse or a spider, I catch them and release them. I’ve made sacrifices both personal and financial for the pets we’ve had over the years and I’ve cried right along with my kids when they’ve died.

But when they died, there was no criminal investigation, no autopsy, no funeral or burial. No last will and testament, no affairs to be settled, no casket or cemetery. They were scooped up and sanitarily disposed of, you know why? Because they were animals not human beings.

Twenty-first century humanity where people can’t discern the difference between a human being and an animal. Like George Carlin said: it won’t be long now for the human race. Pack your shit folks, you’re going away.

The debt clock says that the federal government currently has a debt of $28 trillion that must be paid back with interest which means, for all intents and purposes, the US Federal Government is insolvent, bankrupt. This isn’t a joke and it’s not a conspiracy theory, it’s political, economic and mathematical fact regardless how uncomfortable it may make you feel or how unsettling it is psychologically. It is mathematically impossible for them to pay back that debt plus interest and keep the government funded. Even if they taxed everyone at a rate of 100% it wouldn’t put a dent in the debt. Their only option is to continue to borrow more money to pay off the existing debt and interest. This leads to an exponential growth pattern of debt that is an inescapable economic death spiral.

Practically speaking, the government is already in default on its debt, it just refuses to admit it because it would be political suicide so they create a charade, cook the books and engage in some magical financing to keep up appearances of propriety. Continuing to go into debt in order to pay off debt is a political and economic illusion and just postponing the inevitable and making the inevitable consequences that much worse. In 2020 almost half the federal budget was borrowed, so what happens when they can no longer keep up the charade and stop paying their debt and can’t borrow anymore? What happens when the federal budget is cut in half?

Pension funds – historically government bonds have been considered conservative investments and most pension funds include them as a large part of their portfolio. All those funds will lose a large portion of their worth when the government can’t pay them putting retiree’s pensions at risk.

Interest Rates – there is an inverse relationship between bond prices and the interest rates on those bonds. Commercial interest rates are tied to the interest rates on government bonds, so as the demand for and price of those bonds falls due to lack of demand, the interest rates will skyrocket and those with adjustable-rate loans will be forced into default similar to 2007. It will also adversely affect economic investment since the higher interest rates means bank loans will become more expensive and returns on savings accounts will be more profitable. People will choose to save rather than invest in new businesses and new ideas.

Government Contractors – being unable to borrow means the budget will be slashed to bare bones. Government contracts will be cancelled and the employees of those companies as well as all their suppliers will find themselves either under-employed or unemployed depending on what percentage of the business depended on government funding.

Social Programs – without the money to pay Medicare, Medicaid, Food Stamps, subsidized housing and all the other welfare programs that tens of millions depend on, those people will be left with diminished levels of food, shelter and medical care.

State Governments – many state governments receive billions every year from the federal government. The state governments then fund local governments which will also have to slash their spending or go into further debt themselves.

Social Security – the Social Security Trust Fund has no money in it, all it has are government bonds so when the government defaults on those bonds, the trust fund will be worthless. For decades, social security payments have been made with contributions from current workers – a ponzi scheme — but with the diminished work force, contributions will be drastically reduced so social security payments will have to decline.

Foreign Military Bases – without the money to fund foreign bases, they will be closed and the soldiers restationed stateside, the one bright light in the whole fiasco

International – unable to pay their international obligations, foreign governments will withdraw their demand for US goods and for US Dollars.

Taxes – in a desperate attempt to save face, politicians will try to increase taxes and fees across the board but with the diminished workforce the increases will have little effect on revenues while retarding economic productivity even further.

Federal Reserve – the fed has always been known as the ‘lender of last resort’ and in this case it really is. It will be the only institution willing to create money out of thin air and ‘lend’ it to the politicians to continue financing their shenanigans. The continued devaluation of the currency and the governments inability to pay it back will lead to a collapse of the Federal Reserve, the government and the economy.

Conclusion

As the assassins say in the movies: this is happening. Unfortunately, regardless what anyone does now, the die is cast and the outcome preordained. It’s the inevitable outcome of all empires and the US empire is just the latest.

The average life expectancy for men is 77 and for women is 81. With some standard deviation it’s reasonable to say that anyone between 75-85 is expected to be at end of life. Death is a part of life and when you get to this age range your body is simply worn out making you disproportionately susceptible to all forms of disease and body failures. Use your own family as a sample and calculate the average age of those who have died. Average age of my grandparents and parents was 78. All my aunts an uncles were also in their mid to late seventies.

It’s disingenuous to say that someone in this age range died because of CV rather than old age since, statistically speaking, they would have died of something else in any case simply due to their age. Does it matter why grandma died? Would you be happier if it had been flu related pneumonia or an infection from a broken hip or dementia because life had already decided her time was up? It would almost be more appropriate to say that she died despite CV since she lived to a normally expected age even though there is supposedly a new, extremely deadly virus circulating.

It’s simply not statistically valid to count any deaths in this age range as because of CV especially considering there isn’t really any valid scientific way of knowing. If a PCR ‘test’ comes back positive and an elderly person dies then they are automatically categorized as a CV death. But it’s even worse than that since doctors have been instructed that even if the PCR is negative but they ‘believe’ it was due to CV then it is also categorized as a CV death. My 93-year-old father was locked down in his assisted living facility for 8 months, no leaving, no visitors, masks, social isolation etc. Then he goes to the hospital to have his gall bladder removed and remarkably he ‘tests’ positive for CV! Of course the hospital received $13,000 from Medicaid for the CV patient. How can anyone claim a 93-year-old man died of anything other than old age?

The point is that the statistics about this charade cannot be taken seriously and if they cannot then the political restrictions are not scientifically or medically justified. Just think logically, reasonably and use some common sense.

Production means creating market value. Consumption means destroying market value.

Production is the act of taking factors of production (inputs to production) and combining them in such a way that the market value of the outcome is greater than the market value of the inputs separately. If the market value of the outcome is less, then it’s consumption.

For example, take a 2×4 that has a market value of $10 and cut it into smaller pieces to make a chair. Ignoring other costs like nails and glue and time, the builder of the chair will ask at least $10 for the chair. If he can sell it for $15 then he will have produced $5 of market value. If he cannot sell it for at least $10 but he can sell it for firewood at $5, then he’s consumed $5 of market value.

Production is not the act of just doing something. All costs, including opportunity costs, must be considered to determine if the activity was productive or consuming. Any activity that consumes but is claimed to be productive is an economic fallacy known as the broken window fallacy.

To be productive requires certain economic incentives and risks. First of all, the inputs to production must be obtained—and that comes with a cost. Having incurred that cost, the producer now has an incentive to use his inputs as efficiently as possible in order to sell the outcome for a profit. Further incentive comes from the fact that there’s a risk he’s producing something that the market simply doesn’t value so production decisions are made carefully. The market will not tolerate waste.

Since, for a business, everything comes with a cost, producers are careful to ensure that the benefits associated with those costs are at least equal to, if not greater than, the costs. If not, they go out of business and lose all their investment. Even then, more times than not, businesses still fail to be productive. It’s not easy and the market is a harsh regulator.

So, given the costs and risks, why would anyone engage in productive endeavors at all? Because the market value created is their income, their wealth, their productivity to use to trade with others for the things they need like rent, food, electric, etc. It’s basic economic activity that people have engaged in since the beginning of civilization. Each produces what they’re good at producing, consumes some of it themselves, and trades some of it for the other things they need.

Productive activities are only undertaken, however, by those who need to earn their income. This is borne out, for example, by lottery winners who quit their jobs. They no longer have to earn their income, so they no longer have to incur the costs and risks of being productive. This holds true for anyone who has alternative means of acquiring wealth rather than through productivity.

Given this definition of production and consumption, consider that the government doesn’t produce anything, it directly consumes. It is not subject to economic market forces, but rather political forces. It’s in fact economically impossible for the government to be productive and its consumption should be accounted for in any national income equation.

Government obtains its inputs via legislation: taxes, fees, licenses, fines, unlimited borrowing from the FED, asset seizure, etc. In other words, it takes the inputs to what it does, it doesn’t earn them or have to pay for them. Therefore, they have no incentive to use their inputs efficiently. They can always get more by simply raising taxes, creating new taxes, borrowing more, increasing fees, creating new fees, seizing more, etc.They don’t have to earn anything.

There is also no risk in what the government does since risk is shifted onto society via legislation. When the government does something nobody wants and when resources are wasted, there are no consequences. The government doesn’t go out of business and the resources aren’t freed up for other productive endeavors. They are protected by law. When the government borrows absurdly irresponsible amounts of money, society is taxed to pay it back, not the government.

Nor are economic decisions made by bureaucrats based on market demand, risk, or economic benefit analysis but rather by a vote based on political analysis and political expedience.

Given then that the government has alternative means of acquiring wealth, it serves them no economic purpose to incur the costs and risks of engaging in productive activity, similar to lottery winners. They simply take what they want. The United States Postal Service, for example, is $50 billion in the red even though it has a legal monopoly on delivering first class mail, but continues to operate because the government simply takes more money from society and gives it to the USPS, rewarding economic failure and wasting resources.

The government also indirectly consumes in the form of dead weight losses caused by regulation. Taxes, price floors, price ceilings, trade barriers etc. all create an inefficient allocation of resources resulting in economic costs with no economic gains.

National Income Revised

There are a number of different economic measures for the production of a society. There is GDP, GNP, NNP, NI, NNI, and others. This analysis applies equally to all of them, so let’s use national income.

Classically, national income (a measure of national production) is equal to the sum of consumer spending C, investment spending I, government spending G, and net exports NX.

Y = C + G + I + NX

Government spending is included in the equation as a contributing factor to national income, but the government doesn’t have any wealth of its own. As we saw, it doesn’t produce anything. Any money it spends it has to first take from someone who did produce something in the form of taxes, licensing, fees, regulatory fines, or other methods. It’s just a wealth transfer and government spending is just a redistribution of that wealth.

This classic equation for national income assumes that this redistribution is frictionless, that it’s a wash. What the government takes from C, I and NX, re-enters the equation in G, but that ignores the opportunity costs of government redistribution of wealth.

Government redistribution of wealth leads to malinvestment and the misallocation of resources.

When the government builds the bridge to nowhere that nobody wants and which will sit idle after construction, resources are taken away from market productivity and reallocated to the government make work program. It’s tantamount to hiring people to dig a hole and then fill it back up. There’s an opportunity cost associated with those wasted resources.

The government also imposes domestic and foreign trade restrictions on markets such as taxes, licensing, fees, fines, regulatory compliance, barriers to entry etc. all sending erroneous signals to the markets resulting in the misallocation of resources.

The government redistributes domestic productivity to foreign governments like Israel and Saudi Arabia so that wealth leaves the economy.

The government manipulates wages and prices which skew market signals and decisions.

The government spends hundreds of millions on inputs to war which, by their nature, are meant to be destroyed and destroy other resources in the process with no benefit to the economy. They are the epitome of the broken window fallacy of government.

So there’s a qualified opportunity cost of government redistribution of wealth, OC, that deducts from national income that should be included in the equation.

Y = C + I + NX – OC

Federal Reserve Banking System

The equation also ignores the effects of the Federal Reserve on national income.

Real money is productivity. You produce something, consume some of it, trade some of it for things you need and save some of it. Those savings can be consumed or traded at a later date or loaned out as credit and interest charged.

Such a loan, plus interest, can be paid back by the borrower with his productivity and that’s the end of the loan.

If there is a form of money that is highly tradeable in all markets such as gold or silver, then the markets will use it as a medium of exchange in order to decrease the transactions costs associated with bartering.

Federal Reserve notes are not real money, they do not come from productivity. All Federal Reserve notes are debt issued by the Federal Reserve Banking System. They are created out of thin air at the time of the loan and must be paid back with interest. Interest that must also be borrowed over time.

Intuitively we can reason that this means that any loan can never be paid off. That more money will constantly have to be borrowed to pay principle and interest. To demonstrate:

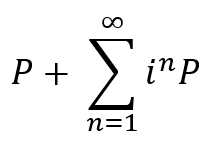

Let’s say the first dollar the fed ever loaned was P and it had to be paid back with interest i so the total debt is P + iP. But iP had to be borrowed too, with interest, since the only money in circulation at the time was P. So the total debt became P + i(iP) and so on. This series becomes P + iP + i(iP) + i(i(iP)) … which is P + over an infinite number of times n.

The series can be shown to converge to P / 1 – i. Mathematical convergence means the sum approaches but never reaches a limit. Economically this means the loan has no limit, it never ends. Moreover, it demonstrates that the greater the interest rate, the greater the value of the convergence limit meaning the more the money supply has to be inflated.

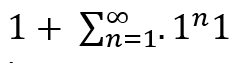

Consider $1 loaned at 10% interest. The total amount of money that would be required to pay the $1 loan back with interest over time due to continued borrowing to pay back principle plus interest converges to:

= 1.11111111111111111… The series converges to 1.11 meaning that it never reaches a limit, it never ends. The debt continues into perpetuity, it can never be paid off. This is true at any positive interest rate.

Consider the following:

P / 1 – i = 0 ;

What conditions would need to be met for the debt to decline over time converging to 0? If P = 0 meaning the original loan was never made in the first place. But if it is made, the debt exists forever. Economically this means that in order to have a money supply society must be in debt. No debt, no money.

The federal reserve – and other central banks — manipulates the interest rate by inflating and deflating the money supply.

If i = 0 in P + iPthen the total value of the debt is just P which can be paid back just by giving P back to the FED whenever. It implies that at i = 0, the money has no value. It can be paid back, it can be held, doesn’t matter. In which case the money is of no use to anyone.

If i < 0 in P + iP then the debt becomes a fraction of P meaning that if P is borrowed, not only is there no interest charged, but you don’t have to pay back all the principle, just a portion of it. In other words, the central bank is giving money away. This money will be wasted for the same reason lottery winners blow their winnings: there’s no costs associated with obtaining the money so anything it is spent on will be of greater benefit than the cost. Any rational person will want the benefits of his actions to at least equal the costs. When the costs are zero, then anything you like is a greater benefit than the cost.

If the federal reserve loaned $1 the amount of money needed to repay the loan at 10% interest converges toward $1.11, more than the original principle plus interest. If they loaned $100 at 10% it would cost $111 to repay the loan. In other words the nominal interest rate is 10% but the effective interest rate is 11% simply due to the nature of the Federal Reserve banking system being debt. The federal reserve imposes an inflation tax on society.

The higher the nominal rate the higher the effective rate and no matter how small the nominal rate is, the effective rate will still be greater.

At a 15% nominal rate, the effective rate for borrowing $1 would be 17.6% and even as low as .5% the effective rate is .502512%

The effect on the money supply and outstanding debt depends on the principle. The greater the principle, the greater the debt required to pay the effective interest.

This means the fed must create money just to cover the difference between the nominal and effective interest rates that serves no productive purpose. It’s money that is not demanded by the market for productive purposes, but which is required only due to the federal reserve banking system. It’s a dead weight loss.

The inflation tax for every dollar borrowed for any interest rate greater than zero can be calculated as: [(i / 1 – i ) – i].

The Federal Reserve Banking System loans money to private businesses and corporations, foreign governments and corporations, and domestic and foreign banks—again creating the money out of thin air and subsidizing failing businesses when they should be allowed to fail and their resources reallocated by the market. Again, rewarding failure.

The Federal Reserve manipulates financial markets, sending erroneous signals about supply and demand in the money markets, creating more malinvestment.

So there’s also a qualified opportunity cost of the FEDs actions, IT, that deducts from national income that should be included in the equation.

Y = C + I + NX – IT – OC

IT is the opportunity cost of the FED imposed on all markets and OC is the opportunity cost of government imposed on all markets.

So the net effect on production of the FED and government is negative. The FED and G consume, they don’t produce anything so the national income equation should be:

Y = C + I + NX – IT – OC < C + I + NX

Conclusion

National income is qualifiably less than its free market potential with a central bank and centralized government. Both consume productivity from the economy.

The claim that the involvement of the government and the FED in the economy stimulates production is nothing but the broken window fallacy in practice writ large. We can see that’s simply not economically possible.

This simple analysis demonstrates the staggeringly destructive effects of Keynesian economic policies that have been imposed on the US economy since before WWII.

All government programs and policies are an illusion; they produce nothing. They simply consume and “the greater good” is worse off for it. It’s impossible for the government or the FED to do anything to benefit the greater good; only markets can do that.

Furthermore, the Keynesian economics being taught in universities is irresponsibly perpetuating this illusion and should be addressed. It’s simply not true.

Simply put, a real economic good is anything that is naturally scarce and in demand. Scarcity implies that you cannot get all of the good that you want freely from nature and there is nothing anyone can do to change that, therefore someone must employ resources and produce it and you must pay for it.

For example, on a sunny Floridian day you can get all the sunshine you want for free by just going outside. Someone doesn’t have to produce sunshine and you don’t have to pay anyone for it. On the other hand, you cannot get all the sun protection lotion you want freely from nature, someone must produce it and you must pay them for it. Therefore, sun lotion is a real economic good. The supply of a real economic good is determined in the market as a function of demand and price.

What is an artificial economic good?

An artificial economic good is a good that is artificially scarce. For example, sunshine on a sunny Floridian day is not scarce, but if someone is locked in a basement with a single window that is controlled by someone else, then sunshine becomes scarce for the basement dweller. If he wants sunshine he must pay someone to open the window and let the sun in.

In other words, a real economic good is a good that is scarce by its nature and always will be regardless of the influence of any outside forces. An artificial good is a good that is not scarce by its nature but because of the influence of outside forces. The supply of an artificial economic good is not determined in the market as a function of demand and price but rather by forces outside the market such as a central committee, a governing board or business rules in a software program. Therefore, supply is unaffected, completely insensitive to market forces.

What is a Bitcoin?

In realty a Bitcoin is nothing more than a text string in a text file that is part of a blockchain. A blockchain is a collection of text files that are related to and mathematically dependent upon one another in an attempt to initially solve the double expenditure problem of digital money.

By its nature, there’s no reason why a computer program couldn’t be written to create text string entries in a text file in a blockchain without end. It’s just a text string so the code could be written to produce bitcoins non-stop ad infinitum, there are no natural barriers to this. Text strings in text files are not scarce by their nature. The only way to prevent that from happening is by choosing to implement constraints in the code to make the supply of Bitcoins artificially scarce by using programmatic forces to influence how many Bitcoins are produced and when. Therefore, Bitcoin is an artificial economic good which is not scarce by its nature but artificially scarce by design. The supply of Bitcoin is not determined in the market by market forces but by business rules in the code and is therefore completely insensitive to changes in demand and price, perfectly price inelastic.

As of today, 6.25 new Bitcoins are created every 10 minutes according to the business rules in the code controlling the supply of Bitcoin. But the programmers who wrote the code could have made that anything they wanted. They could have made it a million Bitcoins per minute or 10-100 Bitcoin per year. The decisions they made for influencing the supply of Bitcoin were arbitrary and meaningless, a centrally planned artificial economic good.

A Bitcoin is a perfectly complementary artificial good with no substitutes

The Bitcoin blockchain is a payment network and a Bitcoin is a perfectly complementary artificial good to the Bitcoin blockchain. In the same sense that a lamp is of no use as a source of light without a lightbulb, you can’t make payments using the Bitcoin payment network without having Bitcoins. But a lamp is a real economic good and can have alternative forms of utility like being used decoratively so light bulbs are not necessarily needed for a consumer to value a lamp. Contrarily, the Bitcoin payment network requires the consumer has Bitcoins and only Bitcoins in order to use it, it is useless without them and there are no alternative uses for it. You can’t send dollars or gold or anything else on the Bitcoin blockchain, only Bitcoins, Bitcoins have no substitutes.

It’s important to make the distinction between what one uses in trade to buy things and how they pay for those things. A blockchain and the entries in it called Bitcoins comprise the Bitcoin payment network. The Bitcoin payment network is a transaction medium that accounts for transactions between users but the price negotiation is always in fiat because goods are valued and priced in fiat, nothing is valued or priced in Bitcoin. Once the price is agreed on, the equivalent in Bitcoin at the moment is calculated and the buyer creates a transaction to the seller on the Bitcoin blockchain for the fiat equivalent of Bitcoins. Fiat was used in trade and the Bitcoin payment network is what is used to pay or send the value of the fiat to the seller. Bitcoins are used as a proxy or token that represent fiat value in order to account for the transaction on the Bitcoin blockchain.

Key point: A payment medium is not the same thing as a medium of exchange.

What is a real medium of exchange?

First and foremost a real medium of exchange is a real economic good which eliminates Bitcoin immediately. Secondly, it’s a good that has emerged from the market a priori as a durable, highly saleable good due to its utility and value across markets. In other words producers and consumers have confidence that its physical nature will resist time and that it will be accepted in trade because it has a history of being traded for its utility and value across markets. Only then will it emerge as a standard measure of value across markets and a medium of exchange. If a good is easily destructible and/or has no history of its saleability across markets, then it won’t emerge from the market as a medium of exchange. Put another way: a real medium of exchange, a real standard measure of value cannot be declared by a central authority, it’s a naturally occurring market emergence phenomenon in which a durable good had utility and value across markets first, only then it emerged as a medium of exchange because of that durability and market utility.

Bitcoin has no utility except as a complementary good to the Bitcoin blockchain which appeared at the same time as Bitcoin. It has no history before the blockchain, it never had utility or value across markets because you can’t take a Bitcoin off the blockchain and use it for anything else.

A real medium of exchange serves as a standard measure of value which means that other goods are priced in terms of it. Nothing is priced in terms of Bitcoin because nothing is valued in terms of Bitcoin. All goods are valued and priced in terms of fiat. When someone agrees to pay using the Bitcoin payment network, the price is quoted in fiat and then converted to the equivalent amount of Bitcoin at that moment. The Bitcoin and the blockchain are the physical vehicle used to account for the transaction but the value of the sale was calculated and paid in fiat.

Opportunity Cost

Investors speculate on all kinds of real goods like gold, silver, land etc. But there’s an opportunity cost associated with holding real goods for speculative purposes. If you buy land, for example, and just hold it hoping the price goes up, rather than farming it, leasing it out or developing it, then you are losing the potential profits from those alternative opportunities. You’re hoping the price goes up enough so you can sell it to cover those opportunity costs plus some profit margin.

That’s not the case with Bitcoin, you either use it to pay for something on the Bitcoin blockchain or you don’t, that’s it. And if you don’t use it on the Bitcoin blockchain then you are holding it and you can sell it any time you want. Of course you want to sell it for at least what you paid if not more so you’ll wait for the price to be right. When you buy something, hold it and then sell it at a later date for profit if possible, that’s speculation whether that was the intention or not. Given the artificial nature of Bitcoin and its disproportionate increase in price relative to real good, the opportunity cost of using it to buy real goods rather than using fiat is so large, it’s not an option. So there is no real alternative to speculating with Bitcoin, there is no opportunity cost to hold it.

In other words, by its nature there are only two things you can do with a Bitcoin: use it on the blockchain or speculate with it but using isn’t an option. If you’re not using it on the blockchain you are speculating.

Key point: This “unintentional” speculative demand is therefore an innate characteristic of Bitcoin.

What is a store of value?

Whether a good is a store of value or not depends on its economic fundamentals since storing value is a long-run phenomenon. The short-run price of a store of value will vary but its fundamentals will ensure that it has value in the long-run that can be used in exchange whatever that value might be at the time.

Key point: a store of value doesn’t mean a high price in the long-run, it means that the good will have a coincidence of value for both the buyer and the seller that can be exchanged at any time regardless what the price is.

A store of value has to be durable so that regardless what happens to it physically, the nature of the good is difficult for the consumer to destroy so it can be used in exchange in the long-run. An ice cream cone doesn’t make a good store of value since the ice cream will melt and all you’ll be left with is the cone. But since gold and silver are fundamental elements, regardless what form or state they are in, they’re still gold and silver. That’s true for any precious metal so precious metals are durable.

A store of value has to have utility and value across markets so that even if it loses value in one market, it still has value that can be exchanged in others. This diversity of value is what insures that the good will be valued in the long-run. Although a bowling ball is durable and difficult for the consumer to destroy its value is limited to the context of bowling and doesn’t have diverse value in other markets. The long-run value of a bowling ball depends on the demand for bowling and bowling alone. If the demand for bowling dries up so does the value of bowling balls so bowling balls don’t make a good store of value.

Gold, silver and other precious metals are durable and have utility and value in a large number of markets: adorning furniture, adorning clothing, jewelry, electrical circuits, heat shielding etc. Precious metals have the sort of durability and market diversity that makes them a good store of value that can be exchanged in the long-run.

Is a Bitcoin a store of value?

Is a Bitcoin durable, is it difficult for the consumer to destroy the nature of it? Kind of an odd question for a text string in a text file but the answer is no. If you keep your Bitcoin wallet on any hardware device – computer, cellphone, memory stick, external hard-drive — and they are damaged beyond repair then your Bitcoins are not useable until you can replace the device and try and recover your Bitcoins from the blockchain with a pass phrase. If you don’t remember your pass phrase or it was on the device that got destroyed then your Bitcoins are most likely gone for good. If you live in an area where you lose electrical power and/or Internet, cellphone connectivity then your Bitcoins are virtually destroyed since you can’t do anything with them, they are worthless which is the antithesis of a store of value.

Does a Bitcoin have diverse market utility and value? No, the only use for a Bitcoin is on the Bitcoin blockchain to transact payments. The long-run exchangeable value of a Bitcoin depends on the demand for people to use the Bitcoin blockchain to transact business. If that demand dries up so does the exchangeable value of Bitcoins.

Speculative value is not the same as exchangeable value. In other words the fact that the price of Bitcoin fluctuates wildly – it lost 80% of its price in one year and 24% in one weekend — isn’t a characteristic of a store of value. The speculative value depends on the speculator not using, not exchanging his Bitcoins on the blockchain but rather continuing to hold them in hopes of recovering from the wild price dips and the price climbing in order to profit from continued speculative demand. A store of value must have value that can be used in exchange at any time in the long-run regardless of the price.

The Supply of Bitcoins

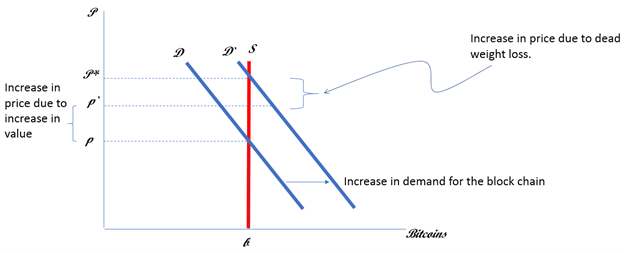

As with all artificial goods Bitcoin has a deterministic, perfectly price inelastic supply, determined outside the market which is completely insensitive to changes in demand and price. It’s programmatically determined so that there is always a discrete number of Bitcoins created every time period. The software is written to manipulate Bitcoin “mining” rates in order to ensure a fixed number of Bitcoins are created every 10 minutes regardless how many “miners” there are. This fixed amount is halved every four years or so. It started at 50, then halved in 2012 to 25, in 2016 it halved again to 12.5 and in 2020 it halved to 6.25. The same amount of Bitcoins are deterministically created every time period regardless of the demand and price. The supply is vertical, perfectly price inelastic in both the short-run and the long-run. It also means that the rate of increase of the supply of Bitcoins is decreasing over time and there’s nothing the market can do to change that.

The Demand for Bitcoins

A blockchain is a real economic good, it’s a data store that must be specified, designed, built, tested etc. just like any software engineering product. There are many commercial uses for blockchain datastores. The utility in the Bitcoin payment network is the blockchain and the fact that all transactions are mathematically related to one another making it difficult to falsify. But since you can’t trade dollars on the blockchain, a perfectly complementary artificial good—a Bitcoin—was created. The original demand for a Bitcoin came from the demand to use the blockchain as a payment system rather than other payment systems like PayPal for transacting financial payments. Being a perfect complement with no substitutes, the fundamental demand for a Bitcoin represents one’s valuation of the blockchain as a payment network and so is a downward sloping curve.

Supply, Demand and Price of a Real Economic Good

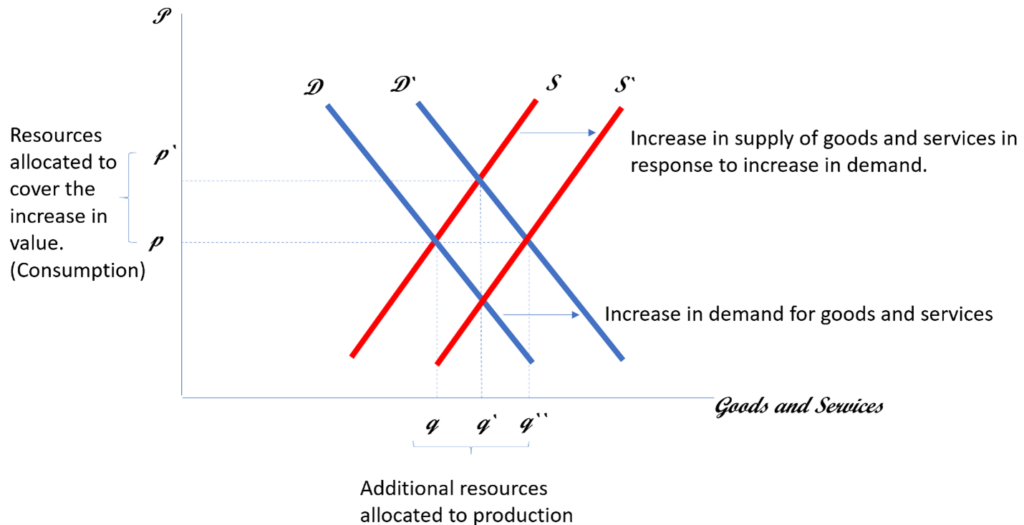

In a market, price indicates the market’s valuation of a good or service. For a real good with an upward sloping supply curve, any increase in demand will result in an increase in price in the short-run for any given level of supply. The increase in price will signal those with unemployed resources that there is potential profit to be made and those resources will be reallocated to increase production and supply in the market. In the long-run this increase in supply will bring prices back down adding a price stabilizing effect to the market.

In other words:

PriceGoods = market valuation of the good or service

Short-run

Long-run

Supply, Demand and Price of Bitcoin

Since the supply curve for Bitcoins is vertical, perfectly price inelastic and determined outside the market, it does not adjust in reaction to an increase in demand and price. The supply of Bitcoin is mutually exclusive from market forces, so the same increase in demand as with a real economic good will result in only an increase in the price of Bitcoins in the short-run with no stabilizing offset in supply in the long-run. In other words the price will go up and just stay there, there is no offset in supply to stabilize it. Part of the increase in price will represent the increase in demand and the rest is a dead weight loss that doesn’t represent value but simply a cost imposed due to the artificial nature of Bitcoins.

In other words: PriceBitcoin = market valuation of Bitcoin + dead weight loss.

Therefore, PriceBitcoin > PriceGoods for the same increase in demand.

This deadweight loss incorporated into the price of Bitcoin accumulates over time reallocating productive resources to non-productive purposes. The price of Bitcoin therefore increases disproportionately to real economic goods due to its artificial nature and it’s this disproportionate increase in price relative to real economic goods that is the catalyst for speculative demand.

Consumption Demand vs. Speculative Demand

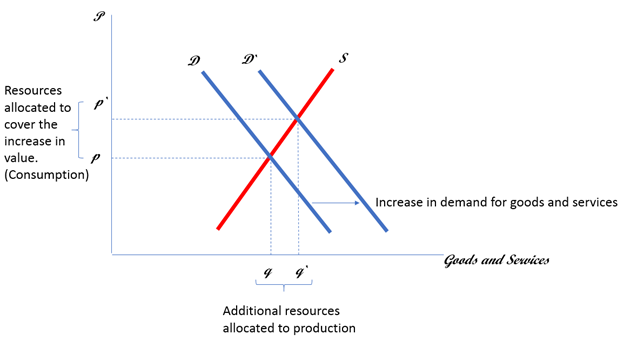

The Federal Reserve has been engaging in what it called “Quantative Easing” since 2009 and in 2020 alone it created 21% of all US Dollars in circulation. When central banks inflate the money supply, the demand for all goods increases. Since the Bitcoin payment network is used to process payments for goods and Bitcoin is a perfect complement for that network, as the demand for goods increased due to the inflation of the money supply, so did the demand for Bitcoins in order use the Bitcoin payment network to pay for them.

Key point: At the same time that the demand for real goods was increasing and driving the increase in the demand for Bitcoins, the price of Bitcoins was increasing disproportionately to the price of the goods they were paying for.

Someone with Bitcoins will see the disproportionate increases in price relative to real goods and choose to hold their Bitcoins rather than trade them for goods with disproportionately lower value. This is because they can always trade for those real goods with cash or some other payment method without having to sell their Bitcoins which are disproportionately increasing in price. Eventually, consumers will substitute alternative payment methods for the Bitcoin payment network which means they’ll hold their Bitcoins which is speculative in nature. At some point speculative demand for Bitcoins becomes greater than consumption demand.

For example: if you have $100 worth of Bitcoin and someone is selling a guitar for $100 and will accept Bitcoin for the transaction then you can pay for the guitar on the Bitcoin blockchain payment network. Then you’ll have $0 in Bitcoin but you’ll have the guitar which you value at $100. If soon after that the price of Bitcoin doubles again as it’s done in the past then you lose out on the $100 profit you could have made if you hadn’t paid for the guitar with Bitcoin. Effectively, the guitar purchase cost you $200 = $100 price + $100 lost speculative profit. It’s more profitable to just pay for the guitar with cash and hold the Bitcoin, then the speculative profit from Bitcoin pays for the guitar.

This is obvious by the disproportionate increase in the price of Bitcoin over the years (figure 1) while daily transactions on the Bitcoin blockchain have remained relatively flat (figure 2) indicating that the overwhelming demand for Bitcoins is not a consumption demand but a speculative demand. People aren’t buying them to use them they are holding them for speculative gains.

In order to manipulate price in the market for a real good, one would have to be able to manipulate both supply and demand which is really impossible to do in any profitable way. But given the artificial nature of Bitcoin and the perfectly deterministic supply, all one needs to do in order to manipulate the price is to manipulate demand which is much easier and done regularly in other artificial markets such as stocks and bonds.

One of the best things about a Bitcoin wallet is that anyone can have one. One of the worst things about a Bitcoin wallet is that anyone can have one, and they do. Government agencies, central banks, corporations, financial whales etc. Those with the financial resources to ‘pump’ up the demand and price and then ‘dump’ their Bitcoins for profit.

Bitcoin exchanges also engage in ‘wash transactions’ where they effectively buy and sell Bitcoins to themselves in order to artificially stimulate demand and price.

Why is the current price of a Bitcoin so high?

As mentioned, the ongoing inflation of the money supply by the Federal Reserve increases demand and causes price inflation across all markets. Bitcoin is affected by the fact that the Bitcoin payment network is used to pay for goods which increases demand and the price for Bitcoins.

But, unlike the price of real goods which have price stabilizing mechanisms on the supply side, Bitcoin is a fixed supply which is completely unaffected by increases in demand and price. So for any given level of demand, when price goes up it just stays there, it has nowhere to go, there are no market forces to bring it back down. The price continues to go up as people switch more and more of their consumption demand for all goods to a speculative demand for Bitcoin, a classic financial bubble. That coupled with the demand manipulations leads to a highly risky and volatile long-run price. The price volatility is due to the disproportionate changes in price. Just as the price goes up disproportionately to real goods, that’s the way it comes back down leading to the wild swings in price over the years.

Conclusion

Bitcoin doesn’t possess any of the economic fundamentals to be a real economic good, a store of value or a medium of exchange. The dead weight loss associated with the price of Bitcoin is economic resources being transferred from productive endeavors in order to pay a tax imposed on the price of Bitcoin due to nothing but its artificial nature.